The money supply continues to grow at a torrid rate.

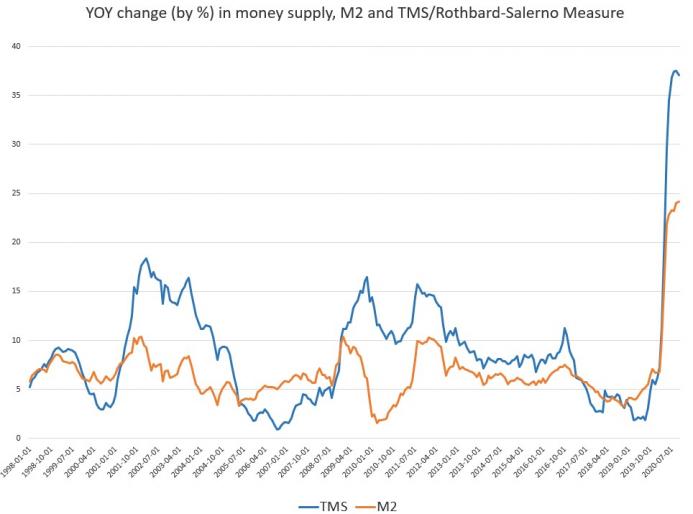

Based on the “true” or Rothbard-Salerno money supply measure (TMS), the money supply grew by 37.08% year-on-year in October. That was down just slightly from September’s record rate of 37.54%.

The staggering growth in the money supply becomes more clear when you compare this year with last. TMS growth in October 2019 was a paltry (by comparison) 4.8%.

Mises Institute senior editor Ryan McMaken said money supply growth is “at levels that would have been considered outlandish just eight months ago.”

The TMS set all-time records eight straight months leading into October. While the TMS metric fell just shy of a ninth straight record month in October, theM2 growth rate did reach historic highs, growing 24.17% compared to September’s growth rate of 24.04 percent. In comparison, M2 grew 6.4 percent during October of 2019.

The “true” or Rothbard-Salerno money supply measure (TMS)—is the metric developed by economists Murray Rothbard and Joseph Salerno, and is designed to provide a better measure of money supply fluctuations than M2. This measure of the money supply differs from M2 in that it includes Treasury deposits at the Fed (and excludes short-time deposits, traveler’s checks, and retail money funds).

The M2 growth rate fell off considerably from late 2016 to late 2018 during the Federal Reserve’s failed attempted to reverse the extraordinary monetary policy it launched during the Great Recession. M2 began growing again in 2019 when the Fed relaunched quantitative easing (although it refused to call it that.) Since March, M2 has followed a trend similar to that of TMS, but to a lesser degree.

Historically, the growth in the money supply has never been higher with the 1970s being the only period that comes close. As McMaken pointed out, the money supply was expected to surge in response to the COVID-19 pandemic as typically happens in the early months of a recession or financial crisis. But it now appears we could be in the early stages of a prolonged economic crisis. Even with the promise of a COVID vaccine, the economy may not bounce back as quickly as many people seem to think. McMaken noted that the Federal Reserve continues to engage in policies that rapidly expand the money supply.

The central bank continues to engage in a wide variety of unprecedented efforts to ‘stimulate’ the economy and provide income to unemployed workers and to provide liquidity to financial institutions. Moreover, as government revenues have fallen considerably, Congress has turned to unprecedented amounts of borrowing. But in order to keep interest rates low, the Fed has been buying up trillions of dollars in assets—including government debt. This has fueled new money creation.”

There is no sign that this extraordinary monetary policy will end them any time soon. As we recently reported, the Fed would need to double quantitative easing in 2021 just to keep pace with the rapidly expanding US debt.

In a recent podcast, Peter Schiff said that stimulus will continue even with a successful vaccine.

The real burden is not the COVID, but all the debt the economy accumulated while the Fed was trying to fight COVID. It’s the COVID cure that is far more harmful to the economy than the disease. So, even after the disease is gone, the cure is going to linger and is going to continue to do damage because we accumulated all this extra debt, because the Fed’s balance sheet is now so much bigger, because the stock market bubble is so much bigger, because the real estate bubble has gained new strength, because everybody has more leverage than they did before.”

To hear Federal Reserve officials, politicians and mainstream financial media pundits tell it – there is no inflation. In fact, the consumer price index remains “stubbornly low” according to those who view rising prices as an economic good. But inflation defined correctly is rampant — it is the expansion of the money supply.

While this record inflationary binge by the Fed has not manifested in significant price inflation as measured by CPI – yet – it has shown up in asset prices – particularly equities. There is no other reason to see record stock market valuations in the midst of a massive economic contraction.

So, why does the mainstream insist there is no inflation? Because it has shifted the definition. It now defines inflation as one symptom of actual inflation. In a nutshell, increases in the price level are not inflation. They are caused by inflation. The government altered the definition to suit its purposes. The common definition used today is nothing more than government propaganda.

")

{kind=link}