“Investing illusions can continue for a surprisingly long time. Wall Street loves the fees that deal making generates, and the press loves the stories that colorful promoters provide. At a point, the soaring price of a promoted stock can itself become the ‘proof’ that an illusion is reality. Eventually, of course, the party ends, and many business ’emperors’ are found to have no clothes.” Warren Buffett (1930- ), America investor, (in his annual letter of Saturday, Feb. 27, 2021).

“All crises have involved debt that, in one fashion or another, has become dangerously out of scale in relation to the underlying means of payment.” John K. Galbraith (1908-2006), Canadian-born American economist, (in ‘A Short History of Financial Euphoria’, 1994).

“History shows that once an enormous debt has been incurred by a nation, there are only two ways to solve it: one is simply declare bankruptcy, the other is to inflate the currency and thus destroy the wealth of ordinary citizens.” Adam Smith (1723-1790), Scottish economist, father of modern economics, (in ‘The Wealth of Nations’, 1776).

***

Over the last few weeks, investors’ sentiment about future inflation and future interest rates has changed. It seems that complacency about inflationary pressures in some parts of the economy is coming to an end.

Even during the economic slowdown brought about by the economic impact of the pandemic, some prices are clearly on the way up. Besides the exuberance in the financial sector where stock and bond prices are frothy, some important prices in the real economy are also strongly increasing.

Sustained price pressures in some important economic sectors

For example, oil prices have increased by more than 50 percent since last year. Construction material prices (lumber, copper, steel, etc.) have skyrocketed by as much as 73% in one year. Because of a strong demand and higher construction costs, real estate prices and rents are rising. For instance, the median home price in the U.S. increased 15% in 2020, while average house prices increased 23% in Canada, during the same period. Food prices have also increased 3.8% in the U.S. and 2.3% in Canada in 2020, and are likely to continue their trend upward in 2021. Even some of the extra liquidity injected into the system has found its way into the cryptocurrency craze, a phenomenon reminiscent of the Tulip mania in Holland in the 17th Century!

The only place where there seems to be little inflation is in the official measures of inflation. In the U.S., the all-items Consumer Price Index (CPI-U) rose only 1.4% in 2020. Even the Producer Price Index (PPI) is up only 1.76% from one year ago. [N.B.: In Canada, the figures are 0.7% (or 1.3% for the CPI excluding gasoline) and 1.4% for durable goods, in 2020].

Currently, the actual inflation rate could be severely underestimated by official figures

Three factors can explain the low inflation reported by official figures. First, one must realize that official inflation indexes are lagging indicators, because important shifts in consumer spending patterns are adjusted every two years. Therefore, during the 2020 pandemic, even though consumers did substantially alter their consumer spending, that shift has not yet been reflected in the official inflation measures.

Secondly, some important sectors (tourism, travel, hotels, restaurants, retail, art and culture, etc.) did experience substantial drops in demand, production and employment, and the prices of their services have declined, artificially pushing the official inflation indexes down. It can be expected that prices in those depressed sectors will bounce back, maybe with a vengeance, once the economic recovery takes hold.

Thirdly, the prices of oil and gasoline were very depressed during most of 2020, and they have since bounced back. Higher energy prices will most probably filter into future measures of inflation.

My tentative conclusion would be that official measures of inflation have seriously underreported the true inflation rate experienced by consumers during the 2020 pandemic.

Many investors have also reached that conclusion. They have realized that the easy-money monetary policies pursued by central banks to boost inflation toward the 2% threshold may have been pushed too far, and that interest rates have been kept ultra low for too long.

This does not mean that more fiscal stimulus is not needed to help workers who have lost their job because of the pandemic and may have trouble going back to their old line of employment.

The clash between central bankers and investors

That is why there has recently been a clash between central bankers and investors about where inflation and interest rates are going to be, once the pandemic is a thing of the past and the economic recovery is well on its way.

The clash pits central bankers, who have been gradually pushing interest rates to ultra low levels with easy-money policies over the last 10 years, and investors, who fear that the after-pandemic economic rebound could be stronger than expected and lead to a resurgence of inflation.

This was epitomized last Thursday March 4, when U.S. Fed Chairman Jerome Powell ruffled investors by declaring that he had no plan to raise interest rates, i.e. not until labor-market conditions are consistent with “maximum employment and inflation is sustainable at 2 percent”. The Governor of the Bank of Canada Mr. Tiff Macklem also seems to subscribe to Mr. Powell’s thesis.

What is the basis for such a clash of perceptions? Essentially, there is a disagreement about how much excess supply there really is in the economy and how robust the economic recovery will be after the pandemic has been vanquished.

On the one hand, central bankers would prefer to keep interest rates on the floor until the economy reaches its full employment level and a higher moderate rate of inflation is attained. On the other hand, investors remember that central banks are known to procrastinate and wait too long to tackle inflationary pressures, ending up overshooting their inflation targets. Indeed, if central bankers wait too long to address inflationary pressures, sooner or later they must step on the monetary brakes, and interest rates shoot up, causing market disruptions.

The pre-1980 period, when central banks waited too long before fighting the creeping inflation, is a good example. In 1980, they pushed interest rates way up, and this brought about the deep 1980-1982 economic recession. [N.B.: In the U.S., the Fed funds rate hit 21% in June 1981, while in Canada, the Bank of Canada interest rate peaked also at 21%, in August 1981.]

Many investors believe that economic conditions are currently reminiscent of what happens after a war, when governments have built up huge debts, and there is a strong pent up demand on the part of consumers who wish to resume spending. By the end of the pandemic, they are forecasting a stronger economic rebound than the one some central banks are expecting.

The Central bankers’ rationale to keep easy-money policies a bit longer

Central bankers presently have two fears, which may explain why they would prefer to keep interest rates ultra low for a few more years.

First, the Fed sees that there are still 10 million fewer jobs today, in the United States, than there were in March 2020. [A similar soft labor market prevails in Canada, as there were 858,000 fewer jobs in January 2021 than in February 2020.] Central bankers think that some structural damage has been done to their economies, especially in the service sector and among young workers, and that it will take time to bring back full employment.

Secondly, the high levels of debt worldwide preoccupy central bankers. Indeed, they see the global financial system becoming overloaded with debt, at all levels, governments, corporations and consumers. They fear that any rise in interest rates would increase the burden of debt service and reduce aggregate demand and, possibly, trigger a financial crisis and an economic recession.

Total global debt is historically very high

Global debt, private and public, is well on its way to reach the unsustainable threshold of 400 percent of global Gross Domestic Product (GDP) in 2021. When interest rates begin rising, this could cause havoc in many ways. Paradoxically, it was the artificially low interest rates of central banks that encouraged such over-indebtedness. And today, those same central banks find themselves trapped in their past policies, and they fear that if they reverted to normal interest rates, it could trigger a global debt crisis.

Indeed, in the aftermath of the Great Recession of 2008, central bankers were very innovative in finding new ways of accommodating politicians who wanted, all at the same time, large tax cuts, higher fiscal deficits, super low interest rates, and faster economic growth, without inflation. This was too good to last for very long.

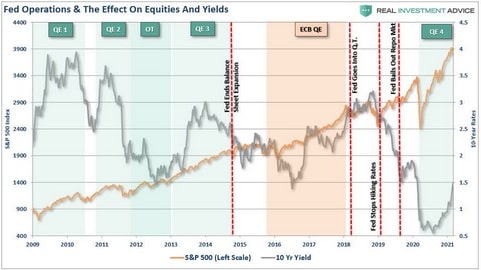

Central banks in Europe, the U.S., and Japan began to load their balance sheets with government bonds and other financial assets, in the hope of controlling both nominal and real interest rates, and, in so doing, boost economic growth. For example, since March 2020, the NY Fed has been buying $120 billion in Treasury bonds in various maturities and mortgage-backed securities each month, in order to keep interest rates ultra low.

The U.S. Fed’s balance sheet of financial assets, which was less than $1 trillion in 2008, now stands at $7 trillion. The Bank of Canada’s balance sheet stood at C$51 billion in 2008 and now is at C$573 billion. – Central banks can do that (i.e. inject large quantities of new money into the economy), for a while, provided that deflationary pressures are such that inflation does not result. If interest rates start rising, the entire policy could begin unraveling.

Attempts to keep interest rates ultra low in such an environment could simply be impossible, without creating unsustainable financial bubbles.

What could happen if central bankers keep interest rates ultra low for too long?

If central bankers nevertheless attempt to keep nominal interest rates artificially low by increasing the money base and the money supply, it would be like adding fuel to the fire. This will create even more inflationary expectations.

Since the mission of central banks is to prevent excessive inflation from taking hold, while keeping employment high, they have to be careful and make sure that an easy-money policy does not generate strong inflationary expectations.

Already, the unorthodox and unprecedented monetary policy implemented during the last decade has created huge financial bubbles in real estate, in the bond market and in the stock market, with little positive influence on the overall real economy.

It’s possible that central banks have been pursuing short-run financial and economic gains at the cost of serious long-run financial and economic pain. Indeed, if they were to persist in creating bigger and bigger financial bubbles, sooner or later, the day of reckoning will take the form of financial crashes.

Will consumers’ extra savings lead to more spending after the pandemic?

It would seem logical to expect that consumers, both in the U.S. and in Canada, and elsewhere, are going to spend at least part of their extra savings, once the pandemic is conquered. Such a pent up demand is another factor that could boost the economy in the next few years.

This could create a period of economic and financial euphoria with booming markets, fueled by the central bankers’ wholesale printing of money, possibly leading into 2023-2024, (provided, of course, that there is no third wave of virus variants).

Extra high public debts will bring about slower economic growth in the future

Because of the economic impact of the pandemic, many governments around the globe are more indebted than ever, even more so than after World War II, with public debts in advanced economies being over 120 percent of GDP, and growing.

Such a high level of over-indebtedness is bound to be a drag on future economic growth. This is because high public debts tend to push long-term interest rates up, and higher borrowing costs discourage private capital investment and hurt productivity. Extraordinarily high public debts may force governments to raise taxes to meet their ballooning debt service requirements, and this could also be another drag on future economic growth.

Conclusion

Economic conditions in most advanced economies, especially in the U.S. and in Canada, but also in Europe, are at a crucial juncture. There is hope now that the pandemic’s economic drag is about to end, because of the widespread vaccination programs implemented in most countries.

However, is it possible that a fear on the part of investors that inflation could quickly rise during a strong economic recovery, might push long-term interest rates way up? Or will central bankers be able to stick to their policies of ultra low interest rates for another year or two? Both outcomes carry their own risks.

Article: The clash between central bankers and investors over inflation and interest rates

")